Saving money in trying economic times can seem like a huge task. Saving your money is not usually portrayed as something glamorous, but it is a necessity for those who accumulate wealth.

Wealthy people have to be good at managing money or at least hire someone to manage their money for them to keep it. Keeping your money requires a different skill set than the one used to make money.

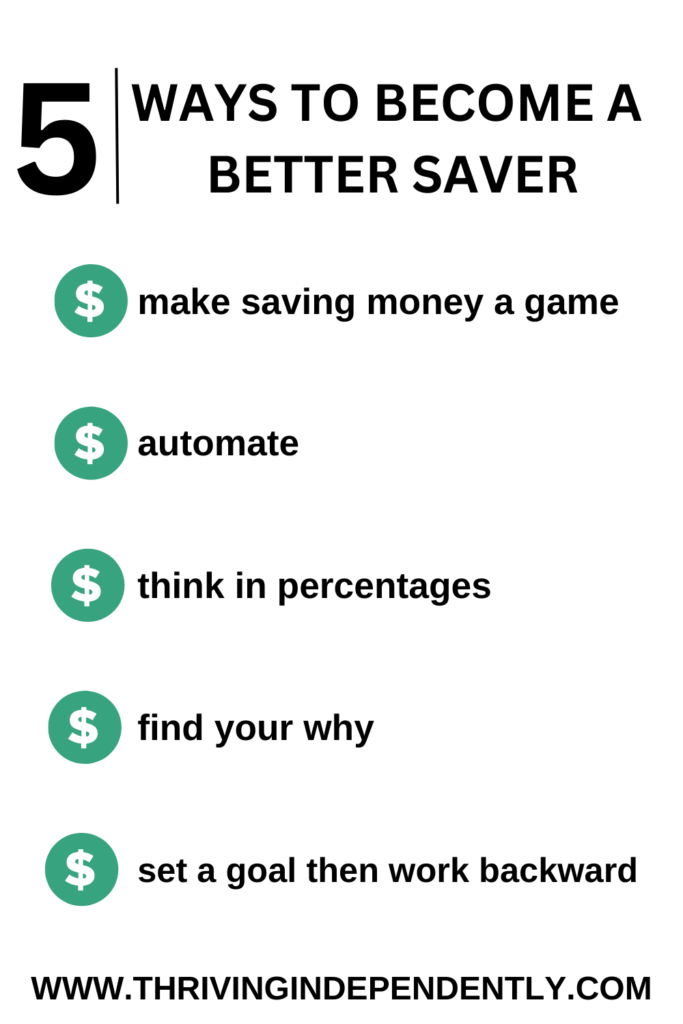

If you want to make the leap to become a better saver and save money faster, here are the things that you should do.

Make saving a game

Saving money becomes fun when you give yourself a way to see it. The goal is to accumulate as much as you can.

Visual elements can carry your journey forward. For example, when schools or churches fundraise, they may have a visual representation of what they have saved.

Some examples of things that you could do are:

- Draw a thermometer and color it in as you reach your savings goals.

- Draw a cloud with raindrops under it and fill in the raindrops when you reach your goal.

- Make an Excel sheet and fill in the cell when you have that amount of money in your bank account.

There are also plenty of free or affordable templates that you can get where other people do this part for you. The ideas are endless! Just type in “savings challenge” in your search bar and you can start from there.

This process does not need to be complicated, it is just to give your mind something else to work off of in the event that seeing a number increase does not motivate you to save.

Turning saving into a game can give you something to look forward to as you earn money. If you know in the back of your mind that you will find more fulfillment in filling in another box to represent your savings, then you may think twice before you decide to make a purchase.

Saving your money is extremely important and you give yourself a great advantage if you can figure out a way to save your money well.

The more automatic the better

Now, I didn’t think that this idea would work because I enjoy seeing ALL of the money I earn flowing in and out of my bank account. But, making something automatic really does make the process easier.

If you have trouble saving money in the past, it may be beneficial for you to interact with it less. At first, you designate the amount that you can allot to each category, then you make the money transfer to your different accounts automatically.

If you take yourself out of the process, there are fewer opportunities for you to forget or intercept the money as it goes on its way. You do not want to allow yourself to be tempted.

Having money leave your bank account automatically is also great because it is mindless. You do not need to decide how much, when, or where more than one time.

You can also look forward to checking back in on balance every once in a while to see how it has grown.

The chances of you missing the money that you put away after a while are small too. If you have always operated off of just the money that you can see regularly, then a slight decrease won’t impact you if you plan accordingly.

You would be surprised about how little you may need to live comfortably. Having the peace of mind that you will be okay financially is also a great source of motivation to have automatic savings.

Change your perspective (percentages)

One thing that helped me a ton in finding value in the little progress that I was making was thinking in terms of percentages.

In the beginning, it is important to save something. No matter the number, you have to save something to build the skill. However, every “something” is not equal.

If I saved 10 dollars every week for 10 weeks, I would have 100 dollars in less than three months. I would look at the amount and get discouraged because it was not as big as I would have wanted it to be.

Something shifts in your mind when you think about percentages. Saving that ten dollars with no context may make it feel insignificant.

But if you earned 100 dollars every week and saved 10 dollars, you’ve just saved 10% of your income! When in June of 2022 according to Zippia, the average savings rate of Americans is 5.1% of their income, you are ahead of the curve!

I believe that effort, in terms of savings, is shown much better in percentages. If you keep track of the percentage of your income that you save over time, you will see the amount you save increase.

As your income increases, your savings will naturally increase too! You won’t feel like you need the extra money because you have already learned to live without it.

You are saving for a better future rather than for some item that you do not know you want to buy yet

A part of becoming a better saver is learning to save for the sake of saving your money. Your money-saving journey will improve when you stop needing a specific reason to save money.

Having abstract reasons like generational wealth and having a secure financial future is good because they account for longevity. Having unassigned goals like these can carry you further.

An example of a poor savings goal would be when I hit $10,000, I will buy xyz. This is considering that the 10,000 dollars you have saved are the only $10,000 that you have.

It is not inherently bad to save for a specific item, it is what many people have to do to get higher-priced items. But If you have something in mind to buy using the money from your savings, you may not be able to keep your savings.

There is a difference between general savings and sinking funds.

Sinking funds are “little savings” that you contribute money to on a consistent basis to buy specific items. For example, you can have a car sinking fund, a beauty sinking fund, or even a tech sinking fund.

The difference between this and general savings is that you intend to buy something with a sinking fund and you use your savings to build wealth.

The issue that I am describing is when people see something they want to buy impulsively, they remember that they have money sitting in a savings account and they proceed to deplete their savings without any prior planning.

I think that people have a greater chance of becoming better savers when they assign their savings as a separate entity that is not to be touched easily. If you set strict terms in the beginning and follow them, a successful savings account is inevitable.

Set a goal and work backward

Building a savings account without intention is a recipe for disaster when you are trying to consistently increase your savings amount. Setting a savings goal can help you stay motivated and push you to do better.

By setting a savings goal and working backward, you are able to see how much is necessary for you to contribute each time period (month, week, bi-weekly) for you to reach your goals.

For example, if you want to save 12,000 dollars by this time next year, you would need to save 1,000 dollars each month and 500 dollars every two weeks to meet your goals.

By breaking it down this way, you can see if it is realistic for you to set these goals and you can evaluate what you need to adjust to reach your goal. You can play with the timeframe, amount, method, and everything else to find what works for you.

When you divide the number, the goal doesn’t seem so huge. Saving $1,000 dollars a month may be more manageable than the thought of saving 12,000 dollars in a year

It’s all about what works best for you and what will get you saving your money. So much money is spent on things that are not necessary every year and savings rates, at least in the United States, are too low.

Becoming a better saver will ensure that you have a healthier financial portfolio and teach you transferable skills. Use these tips to become a better saver today!

For more content like this, you can check out my Pinterest here.

If you liked this post, you’ll love these:

- How to Use Your Tax Refund to Get Ahead Financially

- Easy Ways to Conquer the Poverty Mindset and Welcome Money into Your Life

- Here’s Why You NEED an Emergency Fund Today

Let’s Keep the Party Going!

Don’t forget to follow me on Pinterest so that we can share the knowledge!